Is SaaS Dying? What's Replacing It in 2026

TL;DR: Per-seat SaaS pricing, the model that built a $285 billion software industry, is collapsing because AI agents don't occupy seats, and Wall Street has already started repricing every company still running the old model.

Key Takeaways:

- Between February 9 and February 11, 2026, the SaaS industry lost $285 billion in market value in two days. The S&P 500 barely moved. The market singled out software.

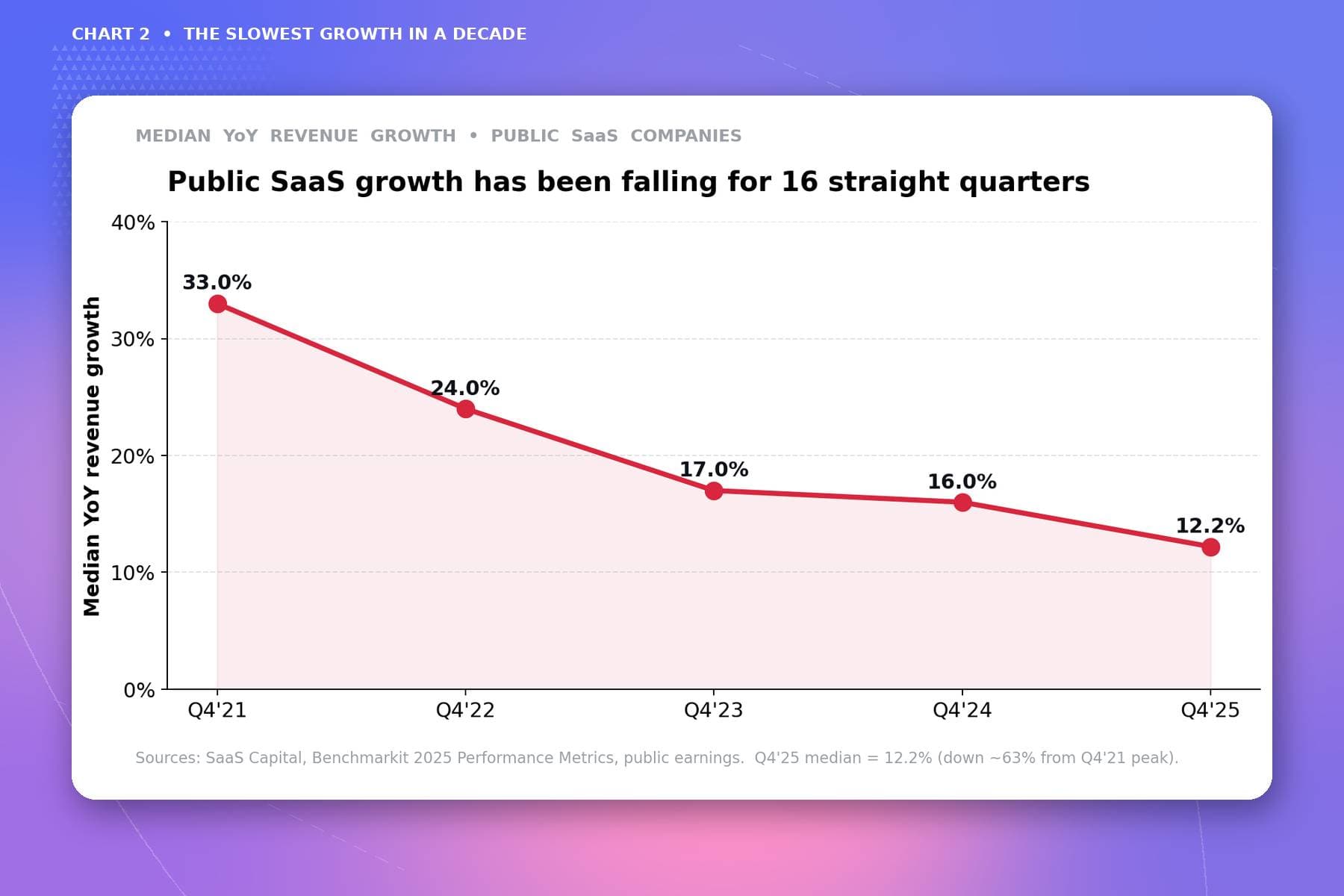

- Public SaaS growth has been falling for 16 straight quarters. Median revenue multiples have dropped from a peak of 37x in 2021 to 26x today.

- AI agents now resolve 53.79% of support tickets without a human. You can't charge a seat fee to software.

- Zendesk's public pricing shows the transition in real numbers: $115 to $155 per seat per month, plus $1,000 to $3,000 for AI Copilot, plus $1.50 per automated resolution on top of that.

- Every major SaaS era has ended this way: not with re-engineering, but with replacement.

Between February 9 and February 11, 2026, the SaaS industry lost $285 billion in market value in 48 hours. Atlassian, Salesforce, and Adobe dropped. The S&P 500 was nearly flat. The market was making a specific judgment about one category of software company.

The frustration had been building for a while. In r/SaaS and founder Slack groups, the same complaint kept surfacing: teams deploying an AI agent that handles most of their support volume while still paying for a full rack of seats.

As one operator put it directly: "Seat-based pricing is a tax on humans. And we just hired fewer humans."

That's what the per-seat SaaS pricing shift looks like on the ground. Not a pricing conference. Not a strategy memo. A company paying for headcount that no longer exists, on a billing model built for a completely different era of software.

This piece lays out the evidence, explains the mechanism, and shows what's replacing it, in the actual numbers.

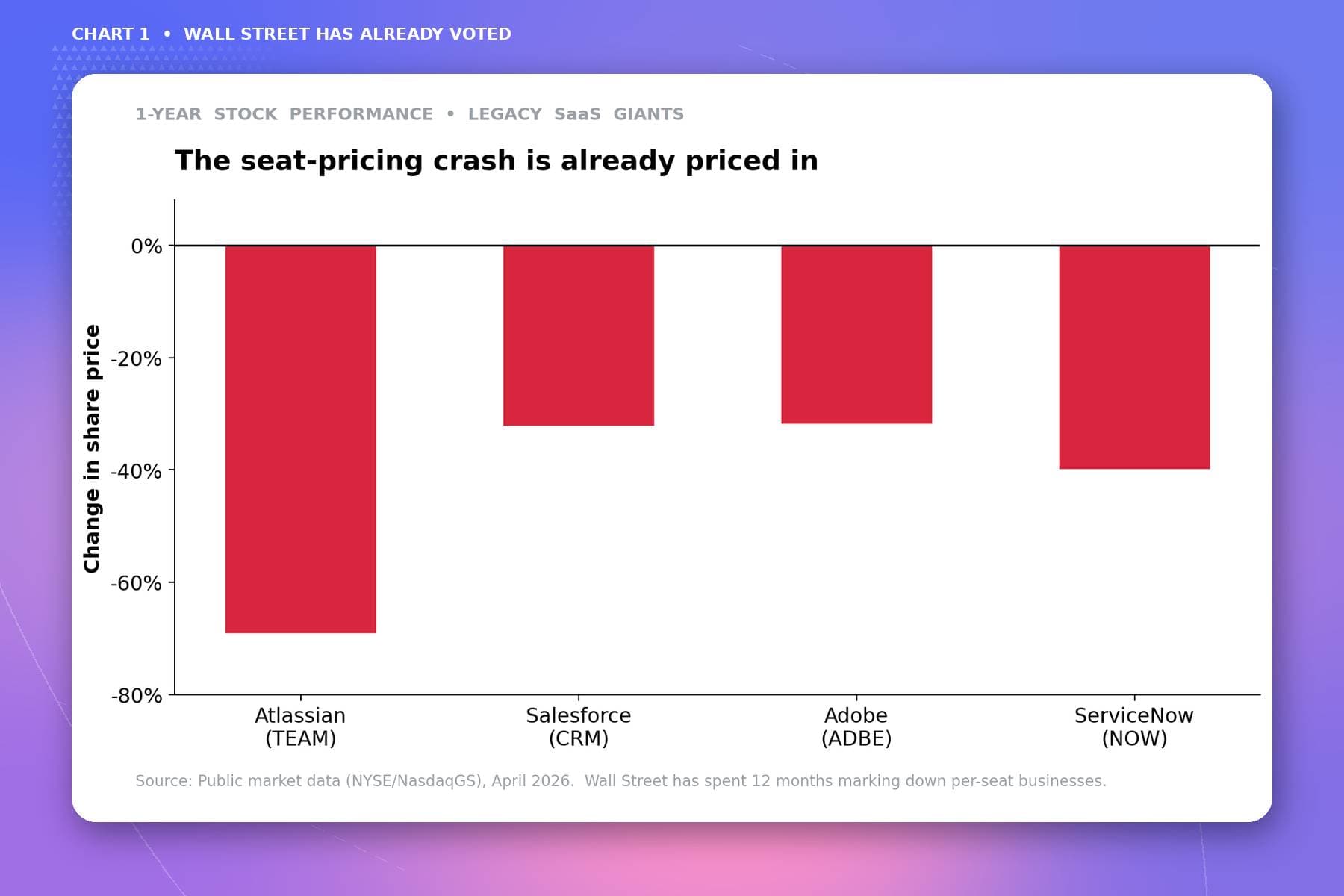

Wall Street Has Already Voted

The February 2026 repricing wasn't random. The financial market was pricing in something specific: the SaaS growth story it had been buying for 25 years had changed.

Public SaaS growth has been falling for 16 straight quarters. That's four years of consecutive deceleration. Median public SaaS revenue multiples hit their peak in 2021 at 37x revenue. Today they sit at 26x. That's a structural repricing.

Atlassian is down roughly 69% since its peak. Salesforce and Adobe are trading near the same window. These are not companies that failed to build good products. They are companies whose pricing model is structurally misaligned with what their software now does.

The S&P 500 barely moved during the same two-day period. The selloff was precise. It landed on software companies that sell seats.

Investors are repricing software companies whose revenue model depends on human headcount growth. When headcount contracts instead of growing, the per-seat model inverts. The vendor gets hurt most when its product works best.

The Cause: Seat Compression

Here is the mechanism that Wall Street was pricing in.

AI agents replaced humans. Fewer humans means fewer seats. Fewer seats means a structurally smaller total addressable market for every software company billing by the user. This is a permanent change in how software creates value and how many people need to touch it.

The layoff data makes this concrete. Oracle cut its workforce by 18% in early 2026. Salesforce cut between 10,000 and 30,000 jobs. Q1 2026 alone saw 60,000 tech layoffs, with roughly half directly attributed to AI agent deployment.

These are companies that built AI capable enough to replace the humans who used to need software seats.

The support category is the clearest example because it's the most measurable. Across customers using AI-native support tools, agents now resolve 53.79% of tickets without a human ever reading them. For well-deployed systems, the threshold sits consistently above 70%.

You paid for seats when humans did the work. AI doesn't get a seat.

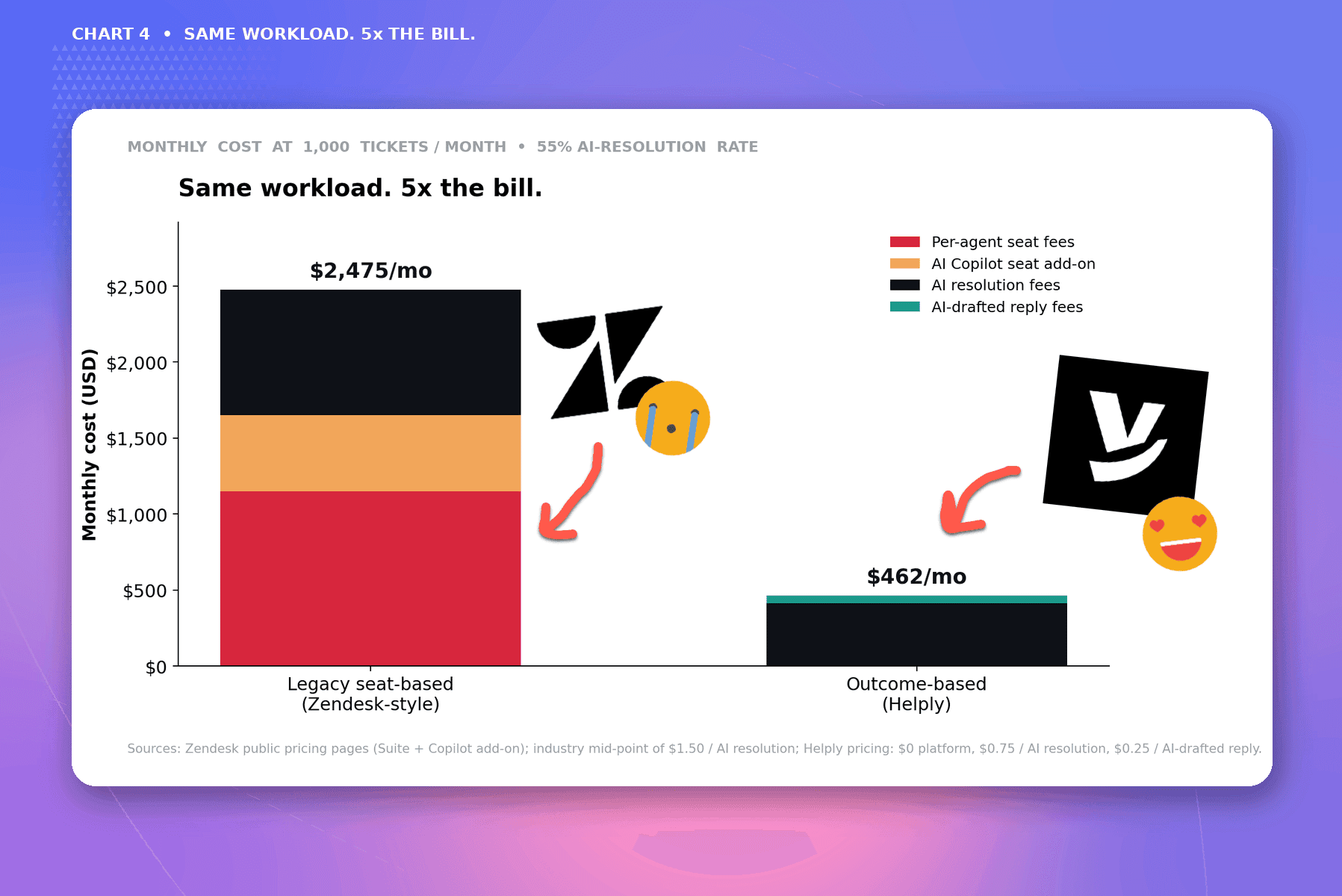

The Receipts: What Zendesk's Pricing Actually Looks Like in 2026

Here is what a team running Zendesk's current pricing structure pays today.

The public seat price runs $115 to $155 per seat per month. That's the base. On top of that, the AI Copilot add-on costs $1,000 to $3,000 per month for the team. Add automated AI resolutions at $1.50 each, and a team handling 1,000 AI-resolved tickets per month pays another $1,500 on everything else.

Seats, plus Copilot, plus per-resolution charges, all running simultaneously. Three billing lines where there used to be one.

This is not a Zendesk-specific problem. Salesforce, HubSpot, Intercom, and Atlassian have all moved toward resolution-based or outcome-based billing layers in the past 18 months. The incumbents can see the same trend the market can.

Their response has been to add outcome pricing on top of seat pricing rather than replacing it, which is why their customers are frustrated and their multiples keep falling.

AI infrastructure costs keep dropping at the same time. MCP (Model Context Protocol) made it effectively free to connect AI systems to external services.

The cost of deploying an AI agent that handles 1,000 support resolutions is a fraction of what it cost to staff 1,000 human-handled tickets.

The gap between what vendors charge and what it costs to deliver the outcome is widening. That gap does not stay open.

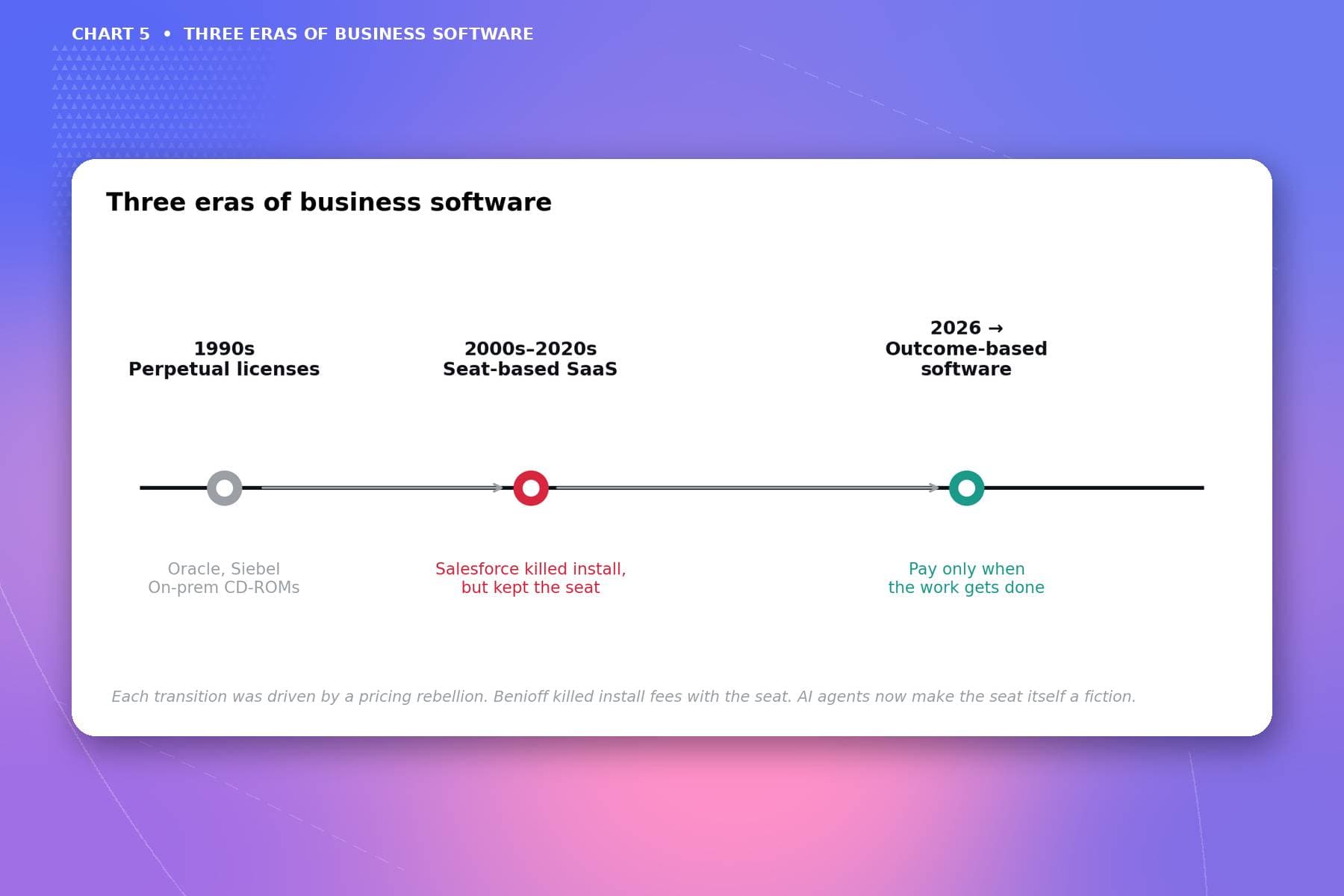

The 25-Year Pattern

This is not the first time a software pricing era has ended. It follows a recognizable pattern.

Oracle and SAP built the enterprise software generation on per-seat and per-server pricing. They dominated for two decades. Then a founder named Benioff stood up at an industry conference with a prop, a "no software" sign, and reframed the entire category. Salesforce didn't re-engineer Oracle. It replaced the model.

The case against Oracle's model wasn't that its software was bad. It was that the pricing had become incompatible with what customers actually needed. No more large upfront licenses. No more per-server fees. Pay monthly per user instead. That was the per-seat model, and it was the right answer for its era.

We are now at the equivalent moment. The per-seat model isn't failing because SaaS companies built bad products. It's failing because the underlying assumption, that software value scales with human headcount, stopped being true.

When AI resolves 53.79% of tickets without a human in the loop, you are not selling a tool that helps a person. You are selling an outcome. Those are different things. They should be priced differently.

Every era of business software has ended with a pricing rebellion. The rebellion isn't coming. Wall Street is already repricing every pre-seat company on Earth. Most people just haven't admitted it yet.

Tomasz Tunguz called it in July 2024:

Salesforce made famous the No-Software mantra competing on pricing. Perhaps usage or performance pricing will be the catalyst for a new era of upstarts displacing incumbents. Maybe we'll see a No-SaaS rebel replicate Marc Benioff's playbook.- Tomasz Tunguz

Kyle Poyar, this April:

"

You can't just sell seats anymore.- Kyle Poyar

Jason Lemkin, February:

When AI can do the work of multiple humans, you need fewer humans. When you need fewer humans, you need fewer seats. This is the quiet killer.- Jason Lemkin

So what comes next?

Wall Street is repricing every per-seat company on Earth.

The smart money is converging on outcome-based pricing as the answer. The incumbents are quietly restructuring their pricing pages and hoping nobody notices.

You can't bolt a new pricing model onto a 25-year-old foundation. The legacy SaaS giants dipping a toe into outcome-based pricing are about to find that out the hard way.

In the next post, we'll lay out what actually comes next (and why every "outcome-based" bolt-on you've seen so far is missing the point).

FAQ

Is per-seat SaaS pricing dead?

It is structurally broken for AI-native workflows. Public SaaS growth has fallen for 16 straight quarters, and median revenue multiples have dropped from 37x to 26x since the 2021 peak.

What is seat compression and why does it matter?

Seat compression happens when AI agents replace the humans who previously needed software seats. Fewer humans means fewer seats, and for any vendor billing by the user, that is a permanent contraction in addressable revenue regardless of how much value the software delivers.

Why did SaaS stocks drop $285 billion in February 2026?

The market repriced companies whose revenue model depends on human headcount growth. When AI shrinks headcount instead of growing it, per-seat billing inverts. The vendor gets hurt most when its product works best.

What is outcome-based pricing and who is using it?

Outcome-based pricing means you pay for a specific measurable result rather than for access or the number of users. Intercom charges $0.99 per resolved conversation. Zendesk charges $1.50 to $2.00 per automated resolution. HubSpot charges $0.50 per resolution. Sierra reached $150 million ARR in 21 months on this model alone.

Why is Zendesk's current pricing so complicated?

Because they layered outcome-based charges on top of an existing seat model rather than replacing it. The result is seat fees plus an AI Copilot add-on plus per-resolution charges running simultaneously: three billing lines where one used to exist.